“I used to pay about a thousand rupees per semester when I did my engineering in 1996”, said our head of technology recently. We were talking about the cost of education these days as he has a couple of young kids, and is planning for their education.

Planning now for your child’s higher education costs will reduce the anxiety you might have to face when the time comes to dish out the money. It’s your bright little one’s job to work hard and get into the institution of their choice, but making sure they can actually afford the education is yours.

All your planning will rest on the following three things:

#1. The amount you will need when your child goes to college

The average fees for an engineering college today (20 years after my colleague went to college) is crossing the 4 lakh mark. For an MBA from a reputed institution, the figure is easily above Rs 10 lakhs. For your children going to college in 10,15 or 20 years, the cost would be much more. Here are approximate costs for some good colleges in Bangalore.

Graduation: approx Rs 1 lakh today, will be approx Rs 7 Lakhs in 10 years and Rs 15 lakhs in 20 years

Graduation (professional courses): today Rs 5-10 lakhs, will be approx Rs 12 Lakhs in 10 years, and Rs 40 lakhs in 20 years

Post-grad: today approx Rs 2 Lakhs, will be Rs 4.5 Lakhs in 10 years, and Rs 16 Lakhs in 20 years

Post-grad (professional courses): today Rs 10 lakhs, will be approx Rs 22 lakhs in 10 years, and Rs 80 lakhs in 20 years

#2. How many years do you have left till your child goes to college

As you can see from above, it matters a lot as to how many years they have till they start filling their admission forms. Not only does it decide how much money you will need, but also where you should invest your money and how much.

#3. Where should you invest this money? or, how much rate of return you will need to work with

After you know how much you need in how many years, the next decision is the actual how. The more time you have the lower the starting monthly investment in the instrument of your choice.

Fixed income investments like FDs and debt funds will give you about 8% (although you have to watch out for the tax impact for FDs); For higher returns, you will need to rely on some investments in equity – typically via equity mutual funds.

Starting early means starting way cheaper – almost half the investment per month

The bottom line:

1.Know what you can afford

2.Start early

3.Don’t touch your retirement corpus to fund this

The smart thing to do

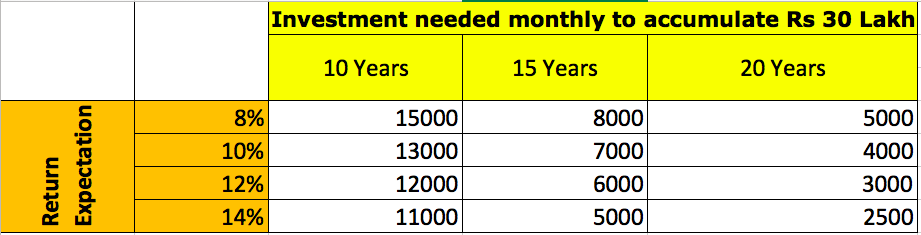

Whether you are an early bird and started saving before or as soon as you got married, or you have barely a decade to go the smart thing to do now is to start a Systematic investment plan in some good equity mutual funds (something like Scripbox long term money) with as much as you can spare apart from the savings that are meant for retirement.

See the chart to get an idea of how much you should invest ideally. If the amounts seem big then, again, go with whatever you can. Trust us, a small amount invested regularly beats not investing at all, any day.

Source -Scripbox.com India Pvt Ltd [IN]